Galleries

How Many People Does It Take to Run a Mega-Gallery? We Found Out

It takes a lot of manpower to achieve global relevance in today's art market—but some galleries have vastly more than others.

It takes a lot of manpower to achieve global relevance in today's art market—but some galleries have vastly more than others.

Artnet News

ShareShare This Article

ShareShare This Article

Galleries are complicated businesses. No two are the same, except in one way: None of them is a public company, meaning that none is obligated to release financial or operational data for all to see. Although the absence of sales and pricing information tends to receive the most attention, this fog makes informed, useful discussions of the industry difficult in a variety of ways.

One of the most consistent (and consistently awkward) of these is our inability to sort galleries into anything but the broadest possible tiers based on size and commercial clout. By necessity, we usually end up resorting to a few well-worn terms to create the taxonomy: emerging galleries, mid-size (or mid-market/mid-level) galleries, high-end galleries, and mega-galleries.

But what do these terms really mean? Are they the best ones to use? And even if so, how do we figure out which galleries qualify for which tier?

It’s common and sensible to try to answer these questions by factoring in publicly available data, like the number of physical spaces that galleries maintain, the number of art fairs they participate in, or the number of artists they represent. Still, these variables can come with heavy caveats—not all fairs are created equal, for instance—and no industry standard exists for how to weigh the information.

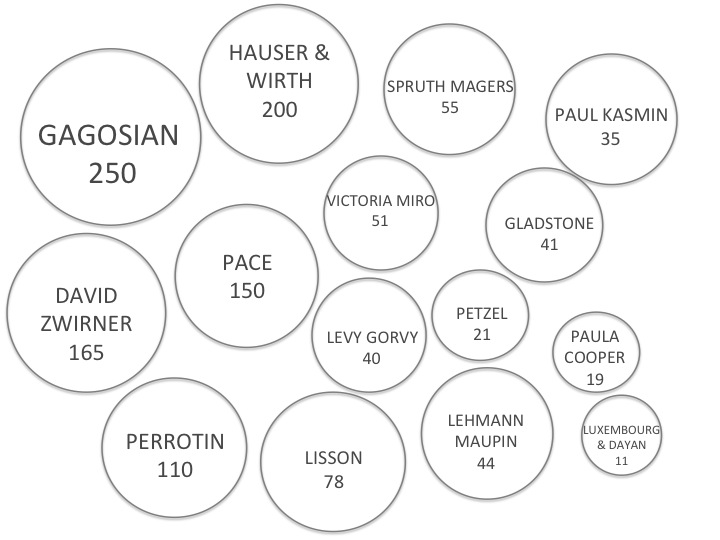

Gallery staff sizes, 2018.

On a macro level, then, the result is that all of us, from journalists to collectors, end up communicating about the gallery landscape in generalities powered mostly by optics and instinct. Like Supreme Court Justice Potter Stewart’s famous statement about pornography, we may not be able to clearly define a mid-size gallery, but we know it when we see it. Still, these broad categories leave out important distinctions—an outcome that helps no one, least of all the galleries themselves.

To tease out the amount of variance involved even at the top of the hierarchy, artnet News collected data from 15 galleries—all of them normally classified as either “mega” or “high-end”—on a relevant but privately held part of their business: staff size. The figures below represent the aggregate number of employees across all locations and departments for each gallery. All data were confirmed on the record by the galleries or their PR representatives.

For context, staff sizes appear alongside the number of permanent physical locations (exhibition spaces or offices) each gallery maintains, and the cities where those locations reside. This information was sourced directly from the galleries’ websites and was current as of publication time.

Obviously, this survey only offers a glimpse of the variances in gallery infrastructure. But it suggests how much nuance can be lost when we fall back on the old stand-by terms—and how much more productive our conversations might be if we knew more.